en

The global investment environment heading into 2026 is quieter, more selective — and full of opportunity for those who know where to look.

After years of relatively cheap capital due to post-covid, expansionary monetary policy and synchronized markets, valuations have reset, discipline has returned, and the drivers of performance have changed. Growth is slower, capital is more expensive, and returns are increasingly shaped by where and how capital is deployed, not by market momentum alone.

Private markets are central to this shift. Real estate is repricing and reopening entry points. Private credit has stepped in where banks have stepped back, becoming a core source of income and stability. Private equity is adapting to longer holding periods, with secondaries and disciplined primaries reshaping portfolios. Venture capital is moving past “growth at any cost” toward quality and fundamentals. Infrastructure is evolving from a defensive allocation into a structural growth engine.

At the individual model portfolio level, the traditional60/40 public markets equity and fixed income framework is no longer sufficient on its own to capture risk and opportunity. Individual investors areincreasingly using private markets to reduce volatility,improve risk-adjusted returns, and access long-term growth drivers unavailable in public markets.

Looking ahead, 2026–2027 vintages mark the early stage of the next private-markets cycle — offering a chance to reset exposures, rebalance portfolios, and compound capital over time. We examine where opportunity is emerging, how capital is being deployed, and the implications for resilient portfolio construction.

By 2026, the global economy looks very different from the rollercoaster of recent years. Inflation has cooled, interest rates have peaked, and the fear of a sharp global recession has faded. Growth is slower, yes — but it’s still there. What’s changed is that it’s no longer evenly distributed, and it no longer comes “for free.”

The days when almost any asset value increased, simply because money was cheap, are behind us. In their place is a more mature market environment, where returns are earned through where you invest, how patient you are, and how well risks are managed.

Interest rates are a big part of this story. While central banks have started cutting rates, they are unlikely to return to the ultra-low levels of the past decade. In simple terms: borrowing will stay more expensive than it used to be and closer to long term averages. For investors, this is actually healthy. Higher rates have pushed asset prices down to more reasonable levels, reduced excessive leverage, and brought income back into focus. Cash flow matters again. Deals need to stand on their own, not rely on rising prices to work.

The U.S. dollar remains the backbone of global investing. Even after periods of weakness, it is still the main currency used for funding deals, buying assets, and moving capital around the world. That said, investors are becoming smarter about currency exposure. As different regions cut rates at different speeds, holding everything in U.S. dollars can become costly from a hedging perspective. More portfolios are now built across multiple currencies, not as a bet, but as a way to improve long-term returns and reduce friction.

Even as the U.S. dollar remains the dominant currency for funding and dealmaking, relative rate paths suggest periods of USD weakness — increasing the case for multi-currency portfolio construction.

Where you invest matters more than ever. The U.S. continues to act as the world’s economic anchor, supported by strong consumer spending, innovation, and corporate investment. Growth is slowing, but it remains more resilient than in most other developed markets.

The Middle East stands out as a rare bright spot. Saudi Arabia and the UAE are seeing strong non-oil growth, backed by large investment programs and improving capital markets. This isn’t just cyclical momentum — it’s structural change playing out over years.

In East Asia, countries like Japan, South Korea, Singapore, and Taiwan are growing steadily, supported by technology and advanced manufacturing, even as global trade softens. China, however, continues to face deeper challenges, with property sector issues and weaker domestic demand holding back growth despite policy support.

2026 is not about chasing the fastest growth or the boldest story. It’s about building a portfolio that can generate income, protect capital, and take advantage of opportunities created by this reset. In a slower, more uneven world, disciplined investing becomes a real advantage — not a constraint.

Despite elevated valuations and structural inflation pressures, markets have remained resilient — supported by AI-driven growth and gradual monetary easing. This is not a cycle for aggressive rate cuts, but one that rewards selectivity and disciplined capital allocation.

Karim Chedid,

Managing Director at BlackRock

Real estate is emerging from a sharp valuation reset after years of cheap financing. As interest rates rose, values adjusted across most markets — not due to weaker demand, but higher capital costs. The result is more realistic pricing and improved entry points for long-term investors. A defining feature of this cycle is the refinancing wall. Between 2025 and 2027, a large volume of low- rate debt comes due. Many assets remain fundamentally sound but cannot be refinanced on prior terms, driving recapitalisations, extensions, and selective distress — creating opportunity without forced selling.

Many owners are reaching the limits of ‘extend-and-pretend’ financing as low-rate bridge debt comes due. This is creating opportunities to acquire high-quality assets at attractive valuations — not because the assets are broken, but because capital structures need to be reset. With new supply being absorbed and financing conditions gradually improving, we expect discounted entry prices and organic rent growth to drive returns over the next 12–24 months.

Ben Kriegsman

Vice President Capital Markets at Lion Real Estate Group

Sector performance is diverging. Multifamily remains one of the most resilient segments, supported by structural housing shortages and steady demand. Rent growth has normalised, but valuations are now at their most attractive levels in over a decade.

Office markets continue to bifurcate. Prime, well-located, energy-efficient buildings are holding up, while older, secondary stock faces declining demand and falling values. Industrial and logistics remain structurally sound, though rent growth is cooling after several years of strong expansion.

Several niche sectors benefit from long-term demand trends. Hospitality has rebounded as travel normalises, while student housing and senior living are supported by demographics and supply constraints. In these segments, returns are increasingly driven by operational performance rather than market beta.

Retail has also become more selective. Well- located, necessity-based and experiential formats continue to perform, while weaker assets struggle — reinforcing the importance of asset quality and tenant mix.

Looking ahead, capital values across many markets are nearing trough levels. As pricing stabilizes and financing conditions improve, 2026 is shaping up to be an attractive vintage for real estate deployment.

Anchored retail centers with necessity-based tenants continue to be attractive with cap rates generally higher than most asset classes. Tenant occupancy remains high and new supply is negligible, which leads to strong pricing power for owners.

Marc Brutten,

Founder and Chairman at Brixton Capital

Real estate in 2026 is no longer about riding rising prices. It’s about buying well, structuring conservatively, and owning productive, operating assets that generate income in a higher-rate world.

THE OPPORTUNITY

In December 2023, Vennre investors co-invested alongside Brixton Capital in a value-add grocery-anchored retail asset in San Jose. Situated in a dense, high-income area with strong links to Silicon Valley, the centre benefits from necessity-led demand and limited competing supply.

THE RATIONALE

Brixton acquired the asset from a dysfunctional JV ownership that let vacancy rise to over 30%. The property was well suited for a repositioning through new ownership and hand-on asset management.

PERFORMANCE TO DATE

- Since acquisition, active asset management has driven results:

- Occupancy reached 94% by end of 2025, materially ahead of the 80% underwritten

- Investor distributions are tracking in line with the 4% annual target

- Value-add initiatives were delivered below budget, supporting returns

Buyers interest has emerged, reflecting market appetite for well-positioned assets

With leasing largely complete, the asset is now entering its stabilisation phase, exactly as envisioned in the original business plan.

Monterey Plaza reflects what works in today’s market: strong fundamentals, operational strength, and disciplined execution. As capital becomes more selective, assets like this are proving more resilient through the cycle.

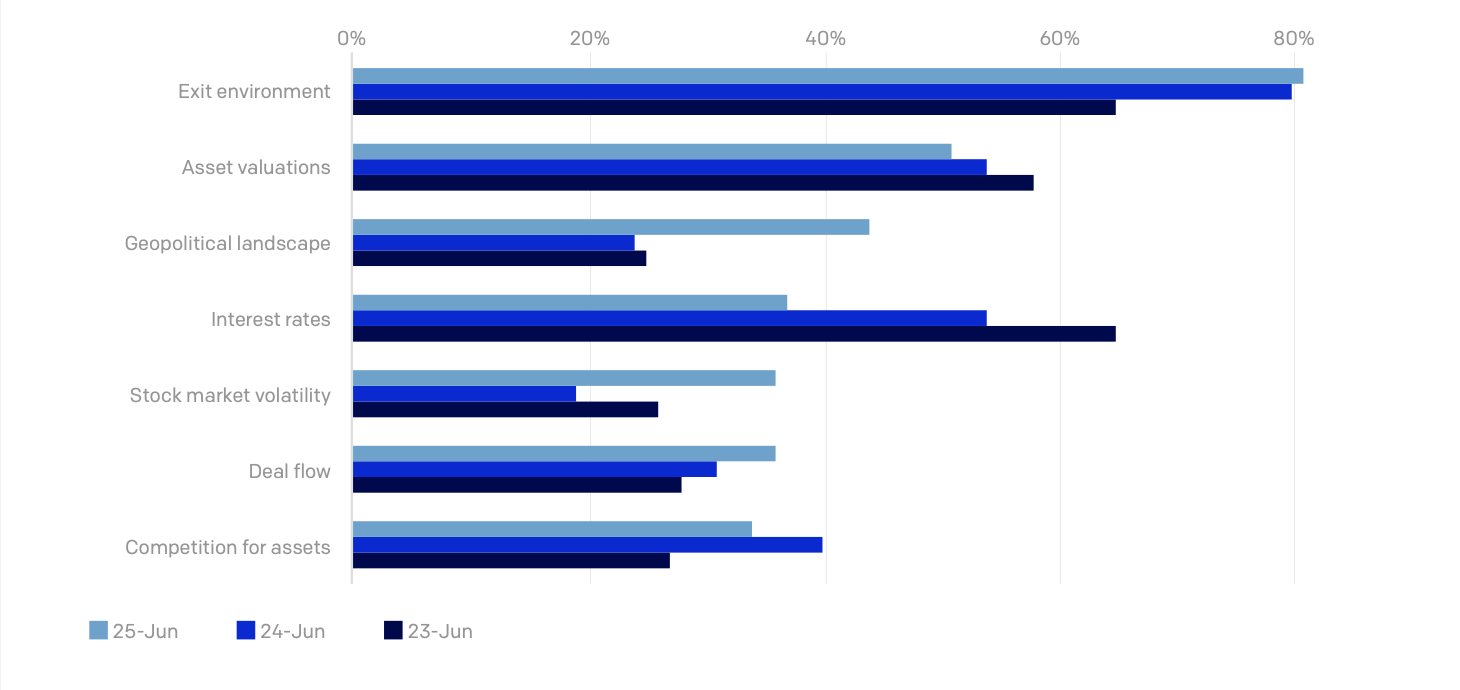

Private equity is built for long-term value creation, not quick exits. But over the past few years, the exit environment has slowed more than expected. Higher interest rates, cautious buyers, and quiet IPO markets have meant that assets are taking longer to sell — even when underlying companies are performing well.

The result is not a broken market, but a timing mismatch. Capital has been invested, portfolio companies are maturing, yet cash is coming back to investors more slowly than in the past.

This has changed how investors think about private equity today. New commitments are still being made, but more selectively and with greater focus on managers who can drive operational growth rather than rely on rising valuations. Returns are expected to come from improving businesses, not just from market momentum.

At the same time, liquidity has become more valuable. With fewer exits, investors are increasingly using the secondary market to rebalance portfolios, manage exposure, and free up capital — without forcing companies to be sold at the wrong time.

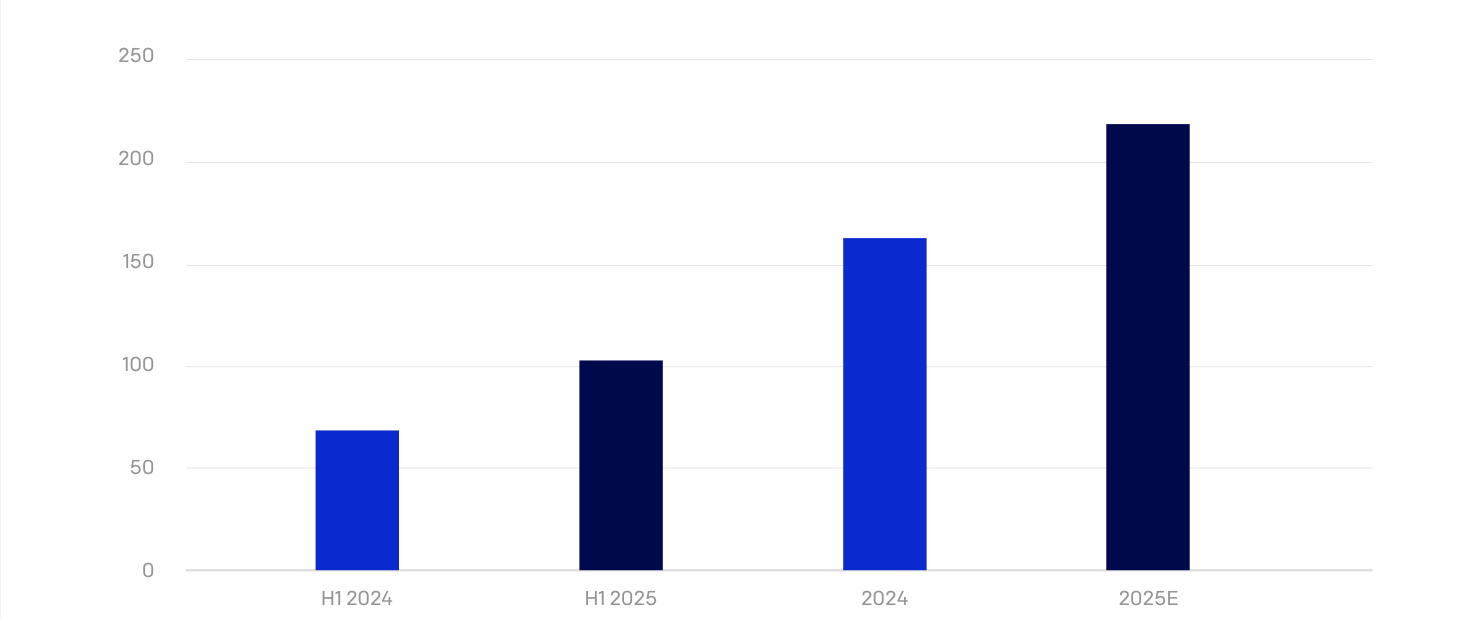

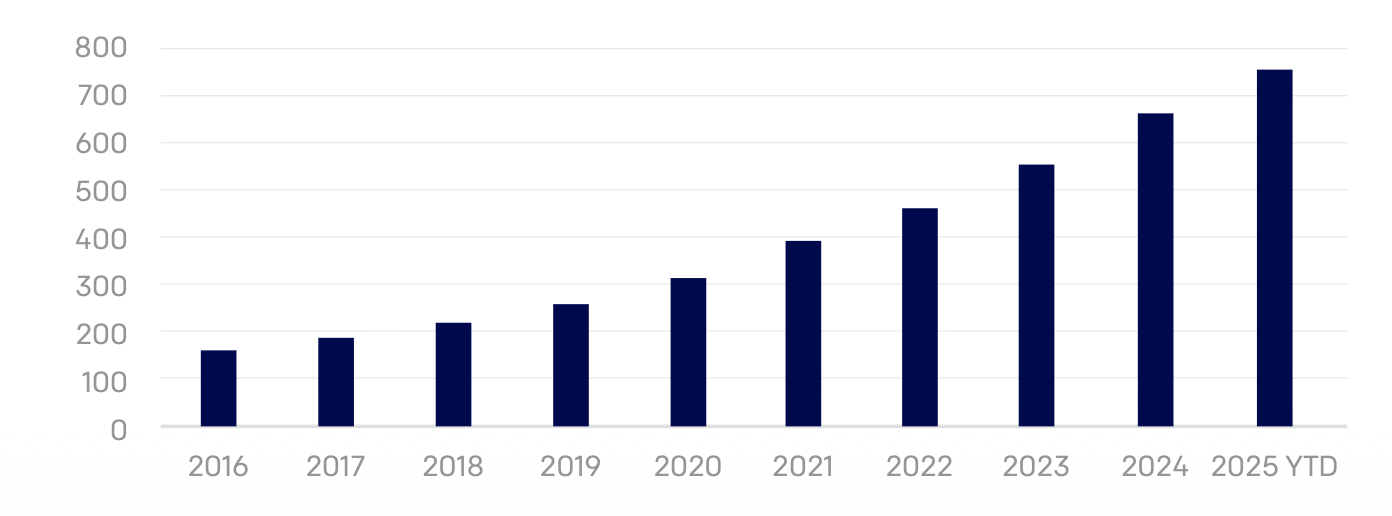

Secondaries are on pace to surpass US$200BN in transaction volume for 2025.

Secondary transactions, where investors buy existing fund interests, have grown rapidly and are now a core part of the private equity landscape. They allow buyers to invest in more mature assets, reduce the early “J-curve,” and gain diversification across companies and vintages. For sellers, they offer flexibility in a slower exit environment.

Investors use secondaries to reduce the J-curve and add diversification. While competition has increased, they remain lower risk than primaries and play an important role in managing liquidity and portfolio construction in today’s market.

Khalil Hibri

Founder and Managing Partner at Tangible Markets

Private equity in 2026 is less about speed and more about structure. Investors who combine patient primary exposure with selective secondaries can stay invested, manage liquidity, and position portfolios for the next exit cycle.

THE OPPORTUNITY

Vennre investors co-invested alongside ACE & Company in its 7th flagship secondaries strategy. As a long-standing platform focused on acquiring mature private equity positions across a globally diversified portfolio.

THE RATIONALE

ASI VII was built to reduce early-stage risk and improve visibility on returns. Instead of investing at the start of a fund’s life, the strategy focuses on acquiring mature fund interests. Typically several years into their investment cycle, where assets are already operating and closer to exit. This allows investors to avoid the early J-curve, benefit from established performance, and gain exposure at attractive entry prices.

PERFORMANCE TO DATE

Since launch, ASI VII has progressed in line with its strategy, building a diversified portfolio of mature private equity assets while beginning to realise liquidity.

- 90 investments acquired across global private equity portfolios

- Exposure to leading managers including

- Blackstone, Glendower Capital, and Carlyle, spanning multiple asset classes and geographies

- 6 exits completed, reflecting steady progress toward liquidity

- Unrealised gross MOIC of 1.8x, demonstrating early value creation

ASI VII shows how secondaries can provide access, stability, and liquidity at a time when traditional private equity timelines have lengthened — making them an increasingly important part of modern portfolio construction.

The venture market has slowed meaningfully since the excesses of 2020–2021. Easy capital has disappeared, exits have taken longer, and liquidity across the ecosystem remains tight. What has followed is not a collapse, but a reset. With distributions delayed and capital locked up for longer, LPs have become more selective. A clear flight to quality has emerged, with established VC firms capturing the majority of new commitments, while first-time and mid-sized funds face a much tougher fundraising environment.

Valuations remain under pressure as investors raise the bar on profitability, efficiency, and sustainable growth. Down rounds are at their highest level in over a decade, reflecting a necessary reset rather than a loss of innovation momentum. Artificial intelligence dominates venture activity, accounting for a large share of global deal flow. Investment is concentrated in infrastructure, semiconductors, and applied AI, with capital increasingly directed toward companies that combine technical leadership with clear revenue paths.

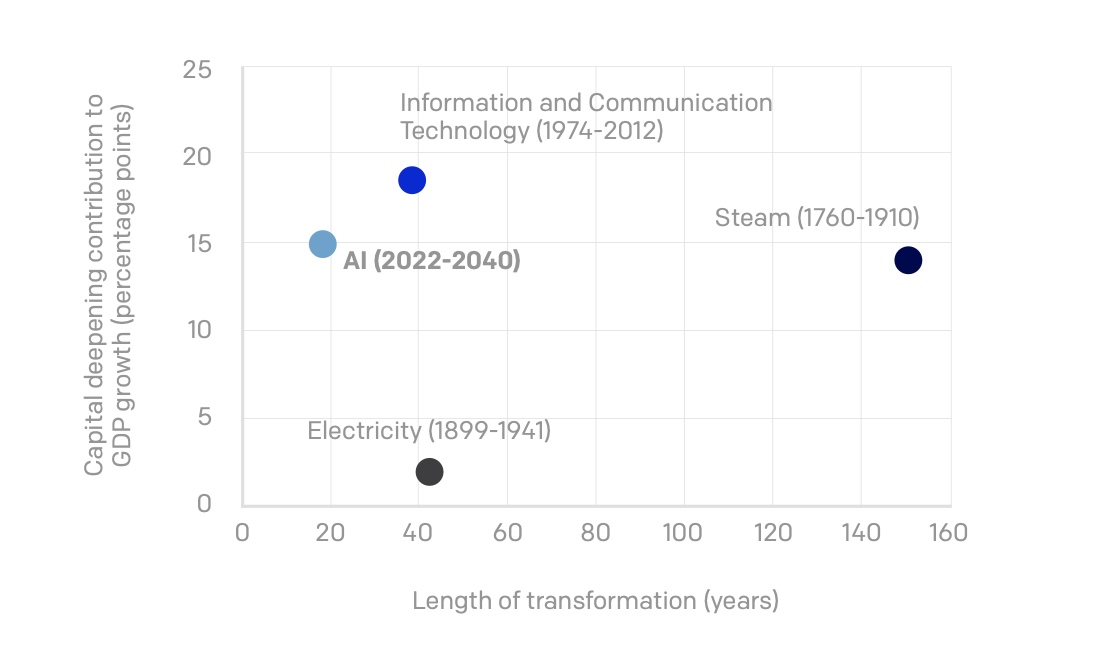

Length and capital deepening of notable innovations, 1760-2040

After a prolonged slowdown, select IPOs and M&A transactions in late 2025 have reopened the exit window, improving sentiment and liquidity expectations. though exits remain more selective than in prior cycles. Looking ahead, long-term themes such as life sciences, defense technology, climate innovation, and applied AI continue to attract durable capital. With valuations reset and discipline restored, 2026–27 vintages are well positioned for attractive long-term performance.

Saudi Arabia is increasingly establishing itself as one of the most active venture markets in the region, supported by strong government backing, improving regulation, and a rapidly expanding pool of local capital.

In 2025, Saudi Arabia led MENA venture funding with approximately $1.7 billion deployed across a record 257 deals — a year-on-year increase of around 145%, making it the most active VC market in the region.

Activity is concentrated across fintech, enterprise software, logistics, and digital infrastructure, supported by continued momentum from Vision 2030 initiatives and growing participation from both regional and international investors.

While the ecosystem remains earlier-stage than the U.S. or Europe, deal quality is improving rapidly. For venture investors, this creates an opportunity to access growth at an earlier point in the market’s maturity — provided manager selection and local execution capabilities are strong.

Venture capital has moved from growth at any cost to quality at scale. As this shift takes hold, Saudi Arabia is emerging as an increasingly relevant venture market for globally oriented investors.

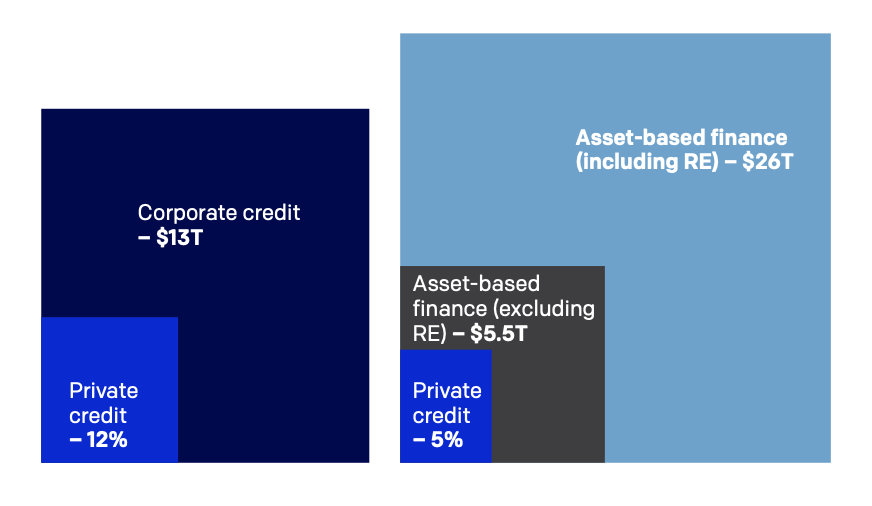

Banks are lending less. Stricter regulation, higher capital requirements, and rising funding costs have made traditional lending, particularly to mid-sized companies, less attractive for banks. This pullback is structural, not temporary, and it has created a durable financing gap.

Private credit has stepped in to fill it, but the market is now entering a more uneven phase after years of rapid growth.

Over the past decade, private credit has grown at an annualised rate of around 14–15%, far outpacing corporate borrowing growth of roughly 5–6%. Assets under management now approach $2 trillion, making private credit one of the fastest-growing segments of private markets.

This growth has coincided with a shift in investor behaviour. With higher rates and slower exits in equity markets, capital has increasingly moved away from traditional buyouts toward income-generating strategies that offer visibility on cash flows and lower volatility.

The market itself has evolved. Direct lending remains the backbone, but unitranche loans, NAV financing, and continuation-fund lending have become mainstream. At the same time, asset-backed and specialty finance strategies are expanding rapidly, offering exposure backed by real assets and contracted cash flows.

As the asset class has scaled, concerns about a potential bubble have grown. However, private credit still represents only around 9% of global corporate borrowing, limiting systemic risk. Returns are expected to normalise from the peaks of 2022, but remain attractive, typically in the 8–10% range, supported by high starting yields and contractual income.

The real risk lies in selectivity. As more capital enters the space, underwriting discipline, deal structure, and diversification are becoming the key differentiators between managers.

Asset-based finance is one area of opportunity where private lenders are just beginning to spread their wings.

Private credit has moved from a niche solution to a core allocation. As banks lend less and investors prioritise income and resilience, disciplined private credit continues to play a central role in portfolio construction.

Infrastructure is stepping out of its traditional role as a defensive, yield-focused asset class. Today, it sits at the center of some of the most powerful long-term trends shaping global investment: energy transition, digitalization, and security of supply.

Capital is following. Infrastructure assets under management now exceed $1.5 trillion and are expected to continue growing at double-digit rates through 2026–27, as governments and corporates accelerate spending on energy, transport, and digital networks.

A key driver is the rapid expansion of AI and data centers, which is placing unprecedented pressure on power generation and grid capacity. Meeting this demand is triggering large-scale investment in electricity generation, transmission, and energy storage, often backed by long-term contracts or regulated revenues.

Sharp Growth in Global Data Center Capacity Demand Driven by AI and Non-AI Workloads...

At the same time, the energy transition continues to attract durable capital. Renewables, battery storage, EV charging, and energy-efficiency projects are increasingly viewed as core infrastructure, supported by long asset lives and predictable cash flows.

Public funding alone cannot meet the scale of required investment. This is creating growing opportunities for private capital through public–private partnerships and hybrid structures, reinforced by policy tailwinds such as the U.S. Inflation Reduction Act, Europe’s REPowerEU, and GCC Vision 2030 initiatives.

Infrastructure is no longer just about stability. It offers long-duration growth, inflation linkage, and contracted cash flows, making it an increasingly essential component of diversified portfolios in the years ahead.

As markets reset, capital is starting to move toward the next set of long-term opportunities. These emerging and niche themes sit at the intersection of technology, demographics, policy, and real-world demand. While still selective today, they offer a glimpse into where private market allocations are likely to expand over the coming years.

THEME 1: AI’S PHYSICAL BACKBONE

AI adoption is driving a surge in investment across data centers, cloud connectivity, and power-ntensive digital infrastructure.

THEME 2: HEALTHCARE BUILT FOR LONGEVITY

Aging populations and medical innovation continue to support long-term demand across healthcare services and life sciences platforms.

THEME 3: DEFENSE, SECURITY, AND RESILIENCE

Geopolitical fragmentation and rising cyber risk are accelerating capital flows into defense technology, cybersecurity, and dual-use assets.

THEME 4: THE NEXT PHASE OF CLIMATE TRANSITION

Beyond renewables, investment is expanding into green hydrogen, carbon capture, and nature-based solutions, early-stage, but gaining traction.

THEME 5: YIELD MEETS REAL ASSETS

Hybrid strategies combining private credit and real assets — such as renewable lending, airplane leasing and data-center finance — are growing in appeal, offering income with asset-backed exposure.

THEME 6: PRIVATE MARKETS GO MAINSTREAM

Evergreen and semi-liquid fund structures are broadening access to private markets for private wealth. At the same time, regulatory developments, including moves in the U.S. to allow limited private-market exposure within retirement plans such as 401(k)s — are gradually expanding the long-term capital base.

THEME 7: STRATEGIC METALS AS PORTFOLIO INSURANCE

Gold is re-emerging as a strategic hedge amid rising geopolitical risk, elevated debt levels, and monetary policy uncertainty. Central bank buying and renewed ETF inflows have supported demand, reinforcing gold’s role as a diversifier rather than a growth asset. Silver offers optionality through industrial and energy- transition demand, but remains more cyclical.

The number of evergreen funds continues to grow rapidly, with total NAV exceeding $400 billion for the first time.

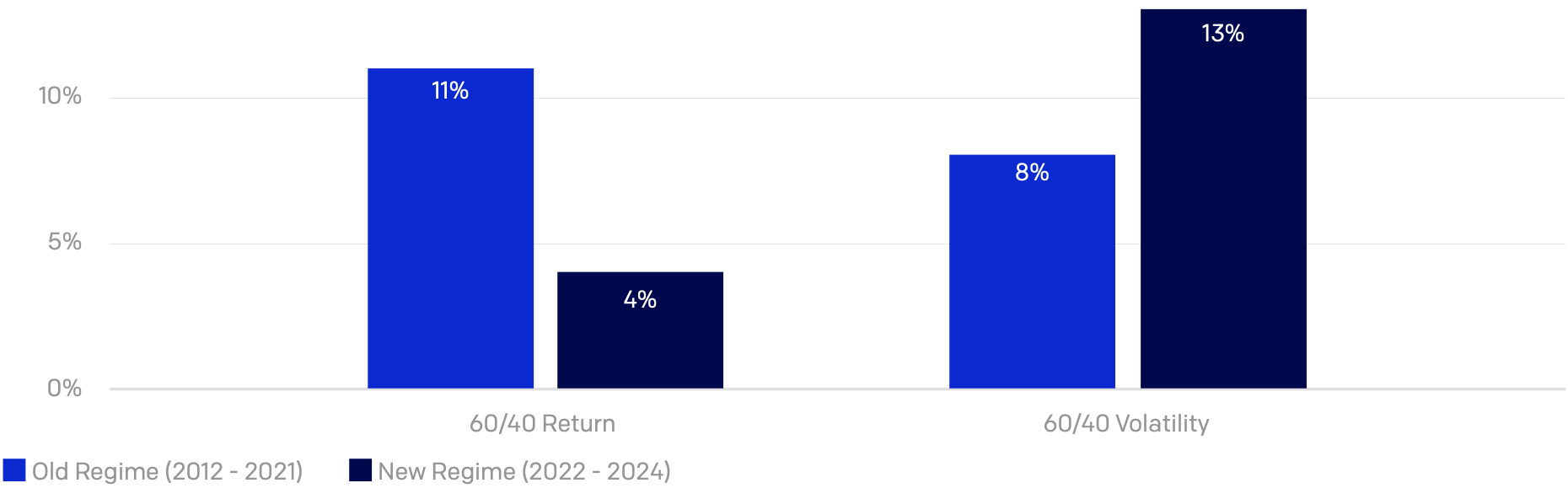

Traditional portfolios built around public equities and bonds, the classic 60/40, were designed for a low-rate, low-volatility world. Today, that environment has shifted. Higher rates, faster market cycles, and more frequent drawdowns make it harder for public markets alone to deliver consistent returns.

As a result, portfolio construction is evolving. Many investors are adopting a 50/30/20 framework, allocating 50% to public equities, 30% to bonds, and 20% to alternatives such as private equity and real estate. Within this mix, private markets provide diversification, more stable cash flows, and access to long-term growth, reinforcing that diversification today is about different sources of return, not just more assets.

Annualized 60/40 portfolio returns and volatility

1. Stability Through Income: The Defensive Engine

Income-oriented private assets (like private credit and core infrastructure) provide predictable cash flows, less drawdown in volatile markets, and the ability to redeploy capital when opportunities arise.

2. Growth Through Fundamental Value: The Offensive Engine

Long-term secular themes (like private equity, venture capital, and innovation in AI, healthcare, and data infrastructure) help portfolios capture compounding growth that public markets may not deliver. Together, these forces help portfolios feel steadier today and grow more tomorrow.

We are entering the early stage of the next private markets cycle. After the high-valuation period of 2020–22 and a reset in 2023–25:

- Valuations are more reasonable

- Competition is less frothy

- Discipline is stronger

- Deal quality is improving

This creates an opportunity to reset exposures, rebalance across vintages, and capture returns as exit markets normalise.

Open-ended and evergreen structures are gaining traction. They allow investors to:

- Stay continuously invested

- Reduce concentration on a single vintage

- Manage liquidity more smoothly than traditional closed-end private funds

This evolution is especially relevant for private wealth seeking longer-term compounding without feeling locked out.

As market dispersion increases, diversification and long-term compounding matter more than ever. Private markets are becoming essential building blocks of modern portfolios.

Karim Chedid, Managing Director at BlackRock

By combining income engines with secular growth drivers, and embracing structures that balance liquidity with optionality, investors can ride through volatility and capture opportunity, not just hope for it.

Modern portfolios aren’t built to be perfect every quarter — they’re built to be resilient across cycles and positioned for long-term growth.

The world entering 2026 is not short on opportunity, but it is more complex, more selective, and less forgiving than the cycle that came before it. Growth is slower, capital is more expensive, and outcomes are increasingly shaped by where capital is allocated, how it is structured, and who is managing it.

Across asset classes, a consistent pattern is emerging. Valuations have reset. Financial engineering has given way to operational discipline. Income, resilience, and quality matter again. From real estate and private credit to private equity, venture capital, and infrastructure, this is a market that rewards patience, selectivity, and long-term thinking.

Private markets play a central role in this environment. They offer exposure to real assets, long-term growth themes, and contractual cash flows that are less tied to daily market noise. When combined thoughtfully, they can help portfolios reduce volatility, generate income, and compound capital over time.

The opportunity ahead is not about making bold, short-term bets. It is about building portfolios that can withstand uncertainty while staying positioned for upside — blending stability with growth, and structure with flexibility.

At Vennre, this is the lens through which we approach portfolio construction:

- Focusing on quality managers

- Allocating across vintages and asset classes

- Balancing income resilience with long-term secular growth

- Using structure and diversification to manage risk, not avoid opportunity

2026 represents a new starting point. For investors willing to lean into this next phase with intention and discipline, the groundwork is being laid for attractive long-term outcomes.